New ETFs Constructed for the FIRE Movement

If you have 20 years until retirement, sure, VTI and chill.

But as you get closer to your fire goals, what about a more permanent portfolio style (also known as risk parity)? And what about an EFT that gives you 4% income yearly to follow the 4% rule?

FIRE ETFs™ made ETFs just for the FIRE movement. They understand that you need to be low cost to be a consideration. Are they low cost? What happens when we look under the hood of these funds?

FIRE ETFs

These ETFs are fund-of-fund ETFs made out of other ETFs already in the Tidal family. So, get this: the ER of the FIRE ETFs is zero until February 2026 (add 0.19 after that). Of course, the funds’ fees flow through, so there is an expense to own them, but for one fee, you get multiple funds packaged with no additional expense. FIRE ETFs run the ETFs.

FIRS FIRE Funds Wealth Builder ETF

At an expense ratio of 0.48, this FIRE fund better do something special. The goal is once you accumulate enough that you no longer want full stock market risk, you can switch to something with less volatility.

It was launched on November 18th, so we don’t have much information yet on flows into the fund.

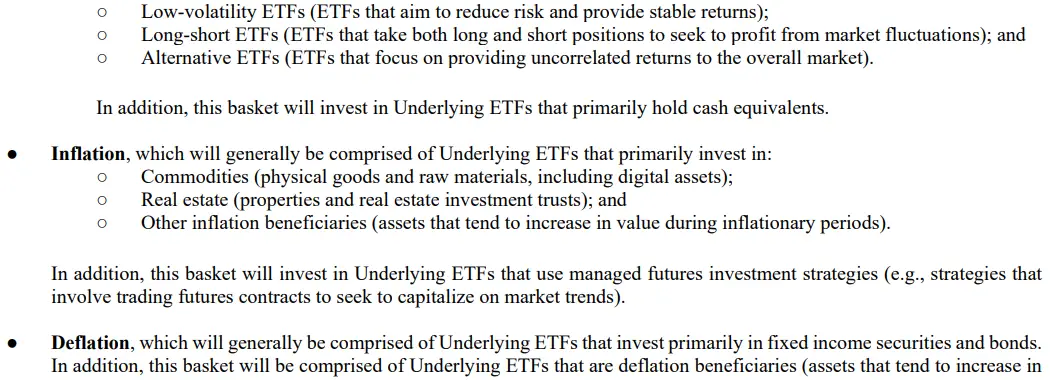

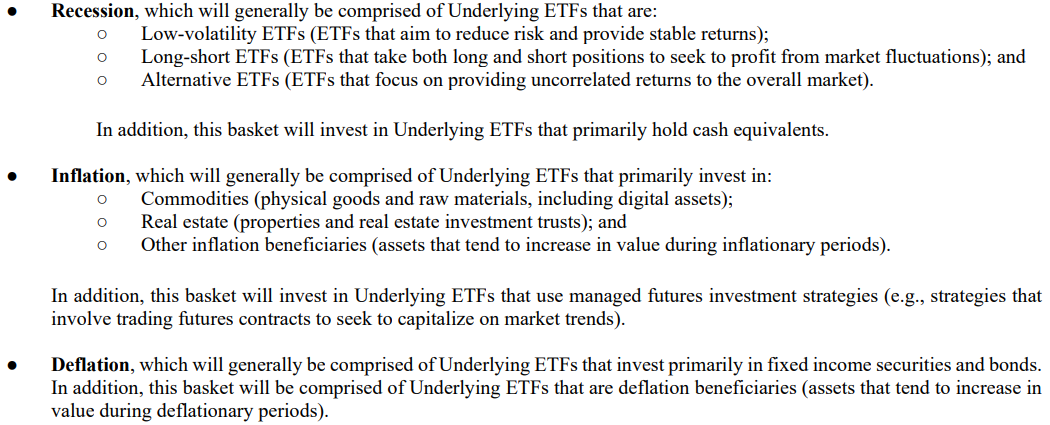

FIRS is an active ETF intended to have a set asset allocation and be used for capital appreciation. Once you are close to reaching your FIRE goal and want to reduce the risk of stock market crashes delaying your retirement (retirement date risk, part of sequence of returns risk before you retire). What is it invested in? Right now there are 17 funds.

Some standouts to me include 7% in bitcoin/gold ETF (a leveraged fund, in which one dollar buys you one dollar of bitcoin and one dollar of gold exposure), another 7% in GLDM (which means you have 7% in bitcoin and 14% in gold), and Meb’s TAIL fund which should do well in a major market correction. There are 10% in bonds, REITs, Pre-merger SPACs (seriously), and cats and dogs.

Their discussion from the prospectus of why they invest in these funds is here.

FIRI FIRE Funds Income Target ETF

At an expense ratio of 0.70, this one better do something special. It is an active ETF whose goal is income and an asset allocation fund. The idea is to give you 4% in annual income (which is not as inflation-adjusted as it should be if you follow the 4% rule, which no one does). Taxation is complicated and depends on the returns you get. Expect ordinary and capital gain income. You will find out how much of each is when you get your 1099 in February or March.

This one only has 13 ETFs inside, and here are the top 10:

I’m actually at a loss for words right now. This isn’t your grandpa’s mutual fund.

New ETFs Constructed for the FIRE Movement

Well, that was fun. It is nice to know that fund manufacturers are paying attention to the FIRE movement and want our money.

I think we will pass.