Managed Futures or Trend Following

Managed futures suffer from a branding problem. Just like high yield is better than junk, and private credit is better than hard money, a rebranding will revive managed futures in the next decade.

However, managed futures are perhaps the best alternative to stocks and bonds. They provide diversification and are largely uncorrelated. Since several ETFs have expense ratios less than 1% (when you used to pay 2 and 20 to a hedge fund for exposure), is it time to add managed futures to your portfolio?

What are Managed Futures?

Managed futures are also known as liquid alternatives or trend following. They are futures contracts on commodities (and interest rates, credit, currencies, etc.), long or short, depending on momentum. Thus, the fund may be long corn and short Euros or any other combination, depending on whether prices are going up or down.

These are quant (quantitative) or rules-based strategies. When the wind shifts, so do the underlying derivatives in the funds.

Managed futures should zig when your portfolio zags. They have performed well under market stress and can be expected to perform over long periods.

When you rebalance or during the withdrawal phase of retirement, it is always nice to have something doing well to pull money from and control risk.

What are the Portfolio Effects of Managed Futures?

Adding ~10-20% of managed futures to your portfolio improves sharp ratios, increases returns, and decreases volatility. It also reduces the maximum drawdown of the portfolio.

What are the downsides of managed futures? Well, in sideways markets, options don’t tend to perform well. These funds have higher expense ratios, and the options degrade over time.

Are Managed Futures Stock- or Bond-alternatives?

I talk about stock-alternatives and bond-alternatives because I like describing asset allocation as risk vs safer assets.

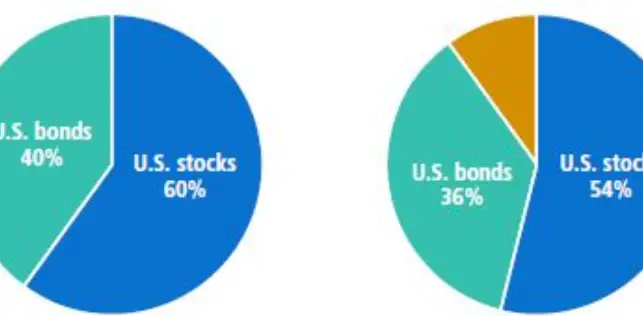

If you invest in managed futures, do you take the money from your stock or bond allocation? Since managed futures are neither a stock nor bond alternative, split the difference.

How to Invest in Managed Futures

Several ETFs can be considered managed futures ETFs.

Let’s look at DBMF as an example (because it is the largest and has performed well since inception compared to the other ETFs). The Expense Ratio is 0.85% (compared to other funds, which range from 0.39- 1.64%). It is based and back-tested on how hedge funds have invested. Most of the money is kept in ballast (T-bills). Since it is based upon trend following, it is a speculation and an investment. Performance is mixed. It performed well in 2022, but nothing beat stocks in 2023. Liquidity is moderate, and there can be wide bid-ask spreads.

Taxes and Managed Futures

You should probably hold any managed future ETF in a tax-preferred account since 60% of capital gains are considered long-term and 40% are short-term. Since you pay ordinary income taxes on 40% of the gains, your IRA is the place to buy DBMF.

Should you Diversify Your Portfolio to Include Managed Futures?

If you are in the withdrawal phase of retirement, diversifying your portfolio with managed futures makes a lot of sense. The time to invest is before, not after, market corrections. I’m considering 10-20% of my portfolio in managed futures, but I’m unsure when I’ll pull the trigger.