Asset Location and Tax-Efficient Investing

How do you allocate assets among your multiple accounts? Tax-efficient investing becomes critical as the size of your brokerage account increases.

How can you optimize asset location? Which funds go into which accounts? How does tax-efficient fund placement improve returns? And how does it affect risk?

First, we need to understand how taxation affects tax-efficient fund placement and the asset allocation of multiple account types. Then, we must understand asset location and where to place our investments.

Multiple Account Types and Tax-Efficient Fund Placement

Let’s examine the different account types most people have available for investing. Our investments are held in different “buckets” or “wrappers.”

Taxable (Brokerage Account)

There are the taxable buckets—our brokerage and savings accounts. Every year, you pay ordinary taxes on interest and short-term capital gains, and you pay capital gains taxes on dividends and long-term capital gains. This is called tax drag.

Tax-Free (Roth)

Next is the tax-free bucket, usually called Roth. You have already paid taxes on these accounts so that you can utilize them in the future without tax implications.

In addition, there are additional sources of tax-free money. For example, you have the basis on your brokerage investments (where you have already paid tax) and loans (on homes, life insurance, brokerage accounts, etc.), where you also get tax-free income. Finally, don’t forget your HSA and some 529 accounts.

Pre-Tax (Retirement Accounts)

Finally, there are pre-tax accounts. These accounts are where the rubber meets the road. IRAs, 401k, 403b, 457 plans are all taxes waiting to happen, ticking time bombs. You don’t own these accounts outright. You own a percentage of them, and the government owns whatever future taxes they decide.

For instance, if you have no other income, you can take money out of these accounts and fill up your standard deduction tax-free. So you put the money in and get a tax deduction—you take it out, and it is tax-free! Brilliant!

But if you have a pension and social security filling up your standard deduction and even your 10 and 12/15% tax brackets, you might pay more in taxes on these accounts in the future than you got in deductions in the past. Not cool, Uncle Sam!

Also, it’s not cool—Required Minimum Distributions. Sam wants his money back, forcing you to withdraw income from these pre-tax accounts once you turn 73 or 75.

What Does Optimized Asset Location Look Like?

Folks are often tempted to locate their assets equally. A poorly optimized portfolio looks something like this:

Above is an example of a 60/40 portfolio. Each account type—the brokerage (taxable), pre-tax (tax-deferred), and tax-free (tax-exempt)—is 60/40. The total net worth is $2.5M.

Why isn’t this tax-efficient?

In the taxable account, you pay ordinary taxes on bond income. Since you have a high enough income to invest in a brokerage account, any ordinary income is tax drag.

Fund your Roth with a higher expected return. There are no bonds in Roths.

A Tax-Efficient Fund Placement Example

Above, now you have all your international equities in your brokerage account. You can take advantage of the tax break from the foreign tax credit.

Also, all your bonds are in a tax-sheltered account with no tax drag. Finally, Roth has all equities with higher expected returns.

Note: To get to 40% fixed income, the tax-deferred account is now 100% in bonds! This lowers the future expected returns and, thus, future taxes. Required Minimum Distributions will be lower, and you can pay less in taxes in the future.

You expect more money in the Roth account because you are taking more risk. Equities are riskier than bonds, but the money will be yours rather than shared with the government in the future. So, you take all the risks and get all the rewards in Roth, and the government shares your risk in retirement accounts.

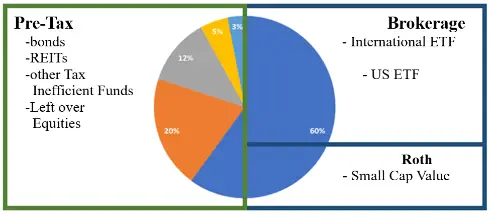

Let’s look at another way to visualize an optimized asset location.

Another Way to Visualize Optimal Asset Location

See above for another example of optimal asset location. Here, the entire portfolio is in one pie graph. This is an excellent example of tax-efficient fund placement!

In this portfolio, 50% of the assets are pre-tax, 40% are in a brokerage account, and 10% are Roth.

The overall asset allocation is 60% equities (blue) and 40% fixed income. Note that blue (equities) has several different types of index fund ETFs, while the 40% fixed income is broken out into several additional funds.

The brokerage account represents 40% of the portfolio in the top right corner. It is tax-optimized in international equity ETFs. The remaining is allocated to US equity ETFs. Remember, you want to use tax-efficient ETFs in the brokerage account rather than mutual funds, which may pay out yearly income (via forced distributions) you don’t want.

In the Roth, 10% of the portfolio is entirely in equities. Consider a small-cap value fund or other “tilt” with higher expected returns.

Finally, the pre-tax portion is 50% of the portfolio total. The last 10% of equities (blue) can be in tax-inefficient equity funds such as REITs, managed futures, or GLDM. This is also where your fixed income goes. Say 20% total bonds, 12% short-term bonds, 5% TIPS, and 3% cash. Or whatever.

Tax-Efficient Fund Placement and Asset Location Optimization

Remember, the government owns part of your pre-tax accounts.

And tax drag: capital gains and bond or cash income drag returns in the brokerage account.

You can optimize your asset location if you don’t lose the big picture—risk. If you can tolerate the risk of having all equities in your taxable accounts—and don’t need the liquidity—you will pay less in taxes. If you can tolerate the risk in your Roth accounts, you will be rewarded with higher expected growth over the decades.

You are usually better off placing funds with higher expected returns in Roth accounts. If you take a risk in your pre-tax accounts, the government shares the risk and gets taxes on the overall return.

With asset location optimization—tax-efficient fund placement—you need to consider future expected returns and tax efficiency.

Sounds like a lot? It is! Retirement income planning—tax-optimized retirement income planning—is a lot to think about.

But you need to start somewhere. If you want a bit easier, read: Visualize the 3-Fund Portfolio Across Multiple Account Types.